The heavy civil construction industry entered 2026 carrying momentum from a strong late-2025 market—but new sentiment data suggests the industry is beginning to shift into a more cautious and uneven environment. While growth opportunities remain available across infrastructure, transportation, and industrial sectors, the broader market is no longer moving in a uniform direction.

Our latest heavy civil construction market outlook 2026 analysis reveals an industry that is rebalancing in real time. Instead of a straightforward expansion or contraction cycle, contractors are navigating a market defined by selective bidding, tighter margins, fluctuating backlog strength, and growing operational pressure.

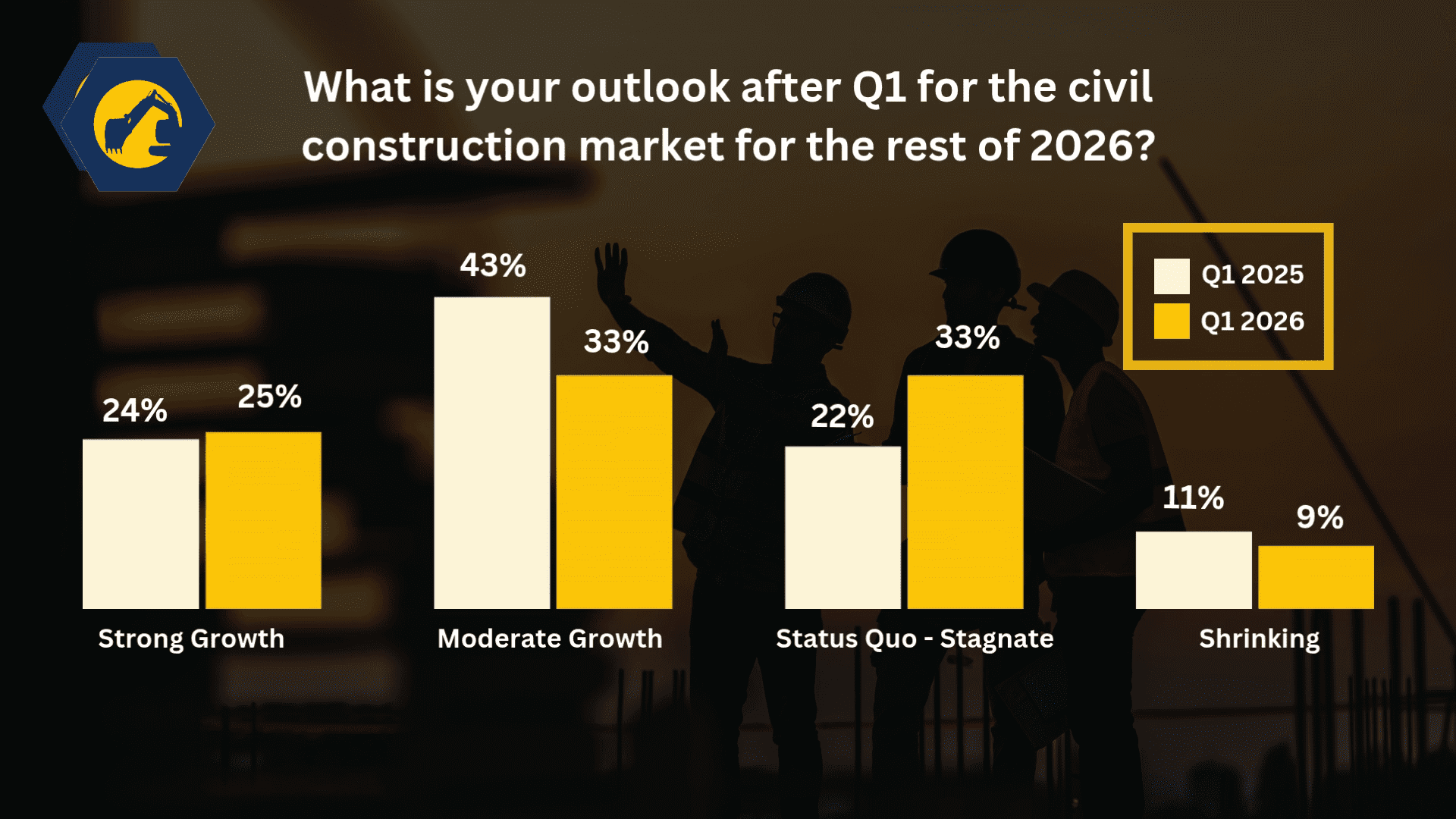

When comparing Q1 2025 to Q1 2026, the data highlights several important changes in contractor sentiment. Firms projecting “Strong Growth” remained relatively stable, increasing slightly from 24% to 25%. On the surface, this suggests confidence still exists among well-positioned contractors with strong project pipelines and healthy backlog visibility.

However, the larger story comes from the decline in “Moderate Growth” sentiment, which dropped from 43% to 33%. At the same time, “Status Quo / Stagnation” increased significantly from 22% to 33%. This movement indicates many firms are becoming more cautious about expansion and are instead prioritizing stability, risk management, and disciplined execution.

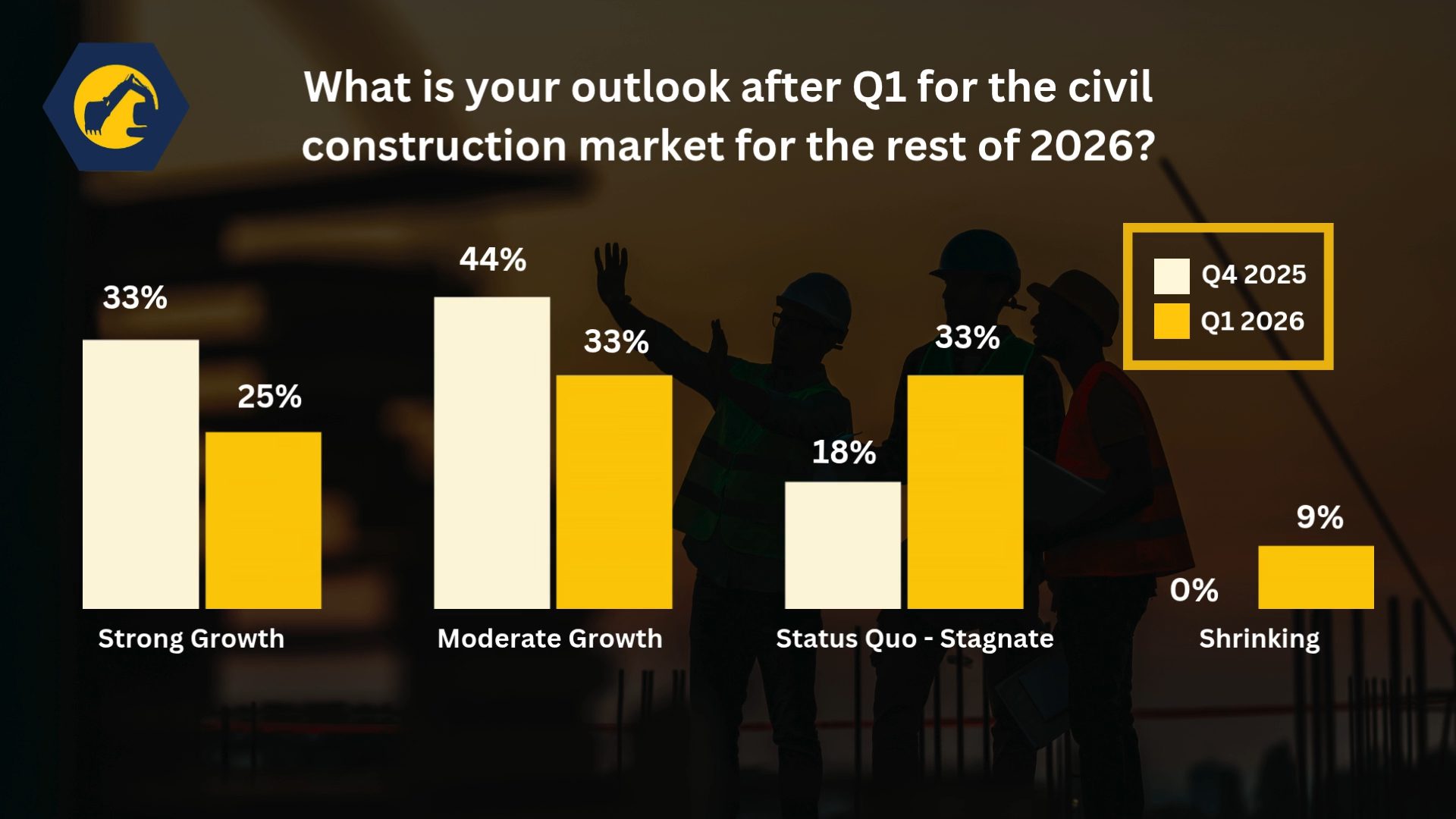

The quarter-over-quarter comparison between Q4 2025 and Q1 2026 reinforces this trend even further. Strong Growth sentiment fell from 33% to 25%, while Moderate Growth dropped from 44% to 33%. Meanwhile, Status Quo / Stagnation jumped sharply from 18% to 33%, and the “Shrinking” category reappeared after briefly disappearing in late 2025.

Taken together, these shifts point to a market that is becoming increasingly segmented. Some contractors continue to experience strong demand and expansion opportunities, while others are facing tighter competition, more selective owners, and slower project movement.

Several external factors are contributing to this transition. Rising material costs, labor shortages, and ongoing supply chain instability continue to create pressure across the industry. In addition, geopolitical tensions and energy market volatility have increased uncertainty surrounding fuel, transportation, and construction input costs. These variables are making forecasting and long-term planning more difficult for contractors and infrastructure stakeholders alike.

Related: https://hcrc.us/2026/04/the-primary-issue-sabotaging-your-talent-acquisition-process/

As a result, many heavy civil firms are reevaluating how they pursue growth. Aggressive expansion strategies are being replaced by more measured approaches focused on protecting margins, maintaining workforce stability, and improving operational efficiency.

This environment is also changing how companies think about hiring and workforce planning. Rather than scaling rapidly at all costs, firms are becoming more intentional about adding key leadership positions, project management talent, and operational personnel capable of improving execution and reducing risk exposure.

The heavy civil construction market outlook 2026 ultimately points toward an industry entering a more disciplined phase. Growth still exists, particularly in transportation infrastructure, bridge construction, utility work, and federally funded projects. However, success will increasingly depend on execution quality, strategic bidding behavior, and the ability to adapt quickly to shifting market conditions.

Contractors that maintain strong client relationships, control project costs effectively, and build resilient operational teams will likely outperform competitors during this next stage of the cycle. Meanwhile, firms relying solely on volume growth without disciplined risk management may face increasing pressure as competition intensifies.

The next 12 to 18 months may not produce the broad optimism seen in late 2025, but they will create opportunities for well-positioned companies that remain strategic, adaptable, and operationally focused. As the market continues to evolve, the firms that can balance growth with discipline will be best positioned for long-term success in the heavy civil construction industry.